Published 20 March 2026

Dental payment plans have become increasingly popular in London, and Denplan is the most widely recognised name in the market. But is a monthly plan actually better value than simply paying for treatment when you need it? The answer depends significantly on how often you attend and what treatment you typically need.

What Denplan Is (and Is Not)

Denplan is not dental insurance. It is a direct payment arrangement between you and your dental practice, administered through Denplan (a company owned by Simplyhealth). You pay a fixed monthly fee directly to your dentist — typically between £15 and £50 per month — and in return, your routine care is included and any treatment you need is discounted, usually by 20 to 25 percent.

Your monthly fee is set by your dentist based on your individual dental health. Patients with straightforward, stable oral health and minimal existing work pay less. Patients who need more frequent monitoring or are likely to require more intensive care pay more. This is one of the key differences from insurance, where the premium is based on population averages rather than your specific situation.

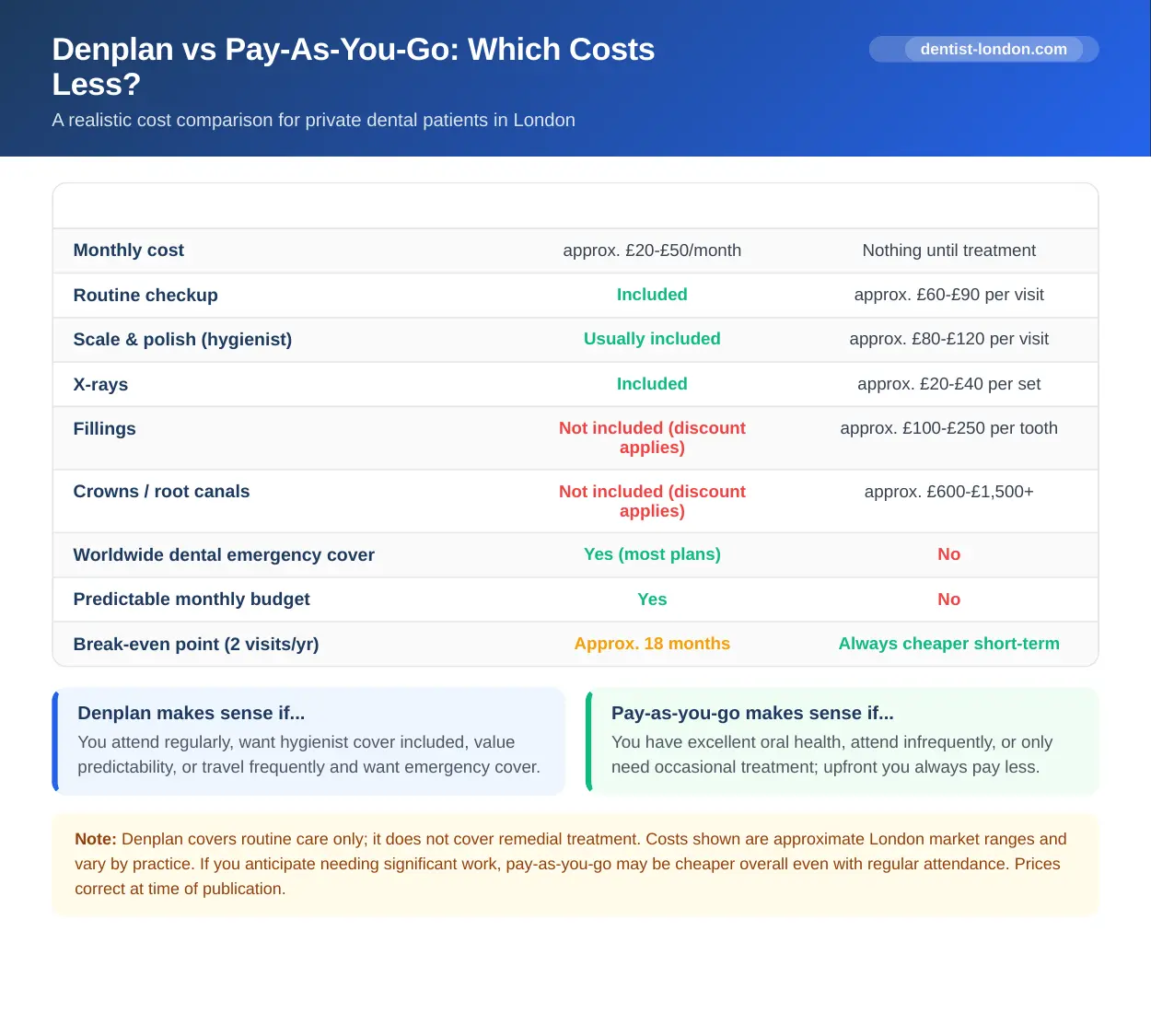

What a Standard Denplan Plan Includes

Most Denplan plans cover:

- Two dental check-ups per year (some plans include one)

- Hygienist appointments, typically one or two per year

- Routine X-rays taken during check-ups

- Emergency dental cover in the UK — usually up to £150 per emergency episode

- Worldwide dental accident and emergency cover

Treatment beyond routine care — fillings, crowns, root canals — is not included, but is discounted for plan members. Cosmetic treatments are excluded entirely from both the included care and the discount in most plans.

Running the Numbers: Pay-As-You-Go vs Denplan

Let us work through a realistic London scenario for a private patient who attends regularly.

Pay-as-you-go costs at a mid-range private London practice:

- Two check-ups per year: £160 to £240

- Two hygienist appointments: £140 to £220

- Total for routine care only: £300 to £460 per year

A Denplan plan for a patient with good dental health: approximately £20 to £30 per month — or £240 to £360 per year — covering those same check-ups and hygienist appointments.

At this level, the comparison is close. Denplan is modestly cheaper for the routine care and adds emergency cover and worldwide accident protection. The financial advantage becomes more meaningful as soon as treatment enters the picture: a Denplan patient needing a £250 filling receives a 20 to 25 percent discount, saving £50 to £62 on that single procedure.

When Denplan Represents Clear Value

A dental plan is most clearly worth it when:

- You attend for two check-ups and at least one hygienist appointment per year — consistently

- You have a history of needing occasional treatment beyond routine care

- You prefer the predictability of a fixed monthly outgoing rather than variable bills

- You travel frequently and value the emergency dental cover included

- Your practice’s Denplan rate compares favourably to their standard private fees

It is harder to justify if you attend infrequently — Denplan only delivers value if you actually use the included appointments — or if you have excellent dental health and rarely need anything beyond a check-up.

The Psychological Value of Predictability

Pure financial comparison does not fully capture one important factor: the value of knowing what your dental care will cost. Unexpected dental bills — particularly large ones for treatment you did not anticipate — cause genuine financial stress for many people. A fixed monthly payment removes the unpredictability from routine care and reduces the impact of treatment costs through the discount. For some patients, this reliability is worth paying a modest premium for, even if the raw numbers are close.

Alternatives to Denplan

Denplan is not the only option in this space. Alternatives include Practice Plan, DPAS, and various independent practice membership schemes that operate without a third-party administrator. The latter often have slightly lower monthly fees because there is no intermediary taking a margin, and the terms can be more flexible. Ask whether your practice runs its own scheme before assuming Denplan is the only route.

Dental insurance — from providers like Bupa, Aviva, or Vitality — works differently: it reimburses costs after treatment rather than covering defined services in advance. Which approach suits you depends on your attendance pattern and your tolerance for the claims process. Our article on whether dental insurance is worth it covers that comparison in detail.

The Practical Recommendation

Before signing up to any plan, ask your practice for a direct comparison: what would your Denplan monthly fee be, and what would two check-ups plus two hygienist appointments cost at their standard private rates? With those two numbers in hand, the decision becomes straightforward rather than theoretical.

For most regular private dental attenders in London who occasionally need treatment beyond routine care, a dental plan represents at least equal and often better value than pay-as-you-go — with the added benefit of emergency cover and financial predictability built in.